Login/Register

Login/Register Supplier Login

Supplier Login

dentsu, a global advertising agency has released a whitepaper profiling CPG consumer behaviour based on an online survey of more than 3,0000 respondents in Southeast Asia. The report details the major concerns and needs of consumers, their current spending habits as to product choices and shopping methods (online, instore, hybrid), priorities and lifestyles, as well as other key information shared by consumers representing different generations. dentsu outlines these findings against the region’s current economic status. Below is piece extracted from the survey:

2024: A challenging year underlined by resilience and opportunity

According to Bain & Company, SEA has weathered global macroeconomic headwinds with more resilience, compared to other regions around the world. Gross domestic product (GDP) growth remains above 4%, while inflation has come down to 3% (relatively low compared to EU, USA and India). Consumer confidence is starting to rebound in H2 2023 after falling to lower levels in H1 2023.1

BCG predicts that rising incomes and growing "high" and "middle" classes (expected to grow at a rate of 5% per annum through to 2030) will continue to fuel consumption.2 The estimated size of the middle-class population in SEA was around 200 million in 2020, and approximately 80 million people of Indonesia's total population were part of the middle class.3

McKinsey’s analysis4 highlights that as incomes rise in Asia, new opportunities for growth in the CPG (Consumer Packed Goods) market are likely to emerge. Premiumisation and societal shifts, such as an aging population, smaller households or women’s economic empowerment, will drive new growth opportunities.

Increasingly many regional consumers are also becoming more environmentally and health conscious. These emerging trends can be addressed by new formats, simpler and more convenient solutions, healthier ingredients and more sustainable products and packaging. At the same time, some brands are tailoring their product and packaging to the growing segment of the population seeking indulgent and premium products.

The impact of inflation

Amid a climate of global economic uncertainty and geopolitical tensions, the region continues to show economic resilience, the average GDP growth for ASEAN-5 (Indonesia, Malaysia, Philippines, Thailand and Vietnam) is expected to increase to 5.3% in 2023 and 5.4% in 2024, and Singapore, 2.2% in 2023 and 2.5 in 2024, based on OECD data.6 However, the OECD highlights several challenges that could have a negative impact on the region’s growth, such as inflationary pressures, the global economic slowdown or supply chain issues. These challenges also have the potential to affect consumers and the CPG market in the region and there are signs of rising consumer confidence, consumers are still impacted by the rising cost of living and inflationary pressures, although this varies by market.

In this context, dentsu has asked SEA consumers how they feel, their main concerns and whether they are down on expenses or planning to cut down on expenses in the next 6 months.

Consumers’ main concerns

The top concerns are local economy, climate change, and unemployment. Malaysian consumers were more likely than the other countries to pick the economy as a concern; while Indonesian consumers were much more likely to consider unemployment a concern.

Concerns about the strength of the economy and their current financial situation were highest in Malaysia and the Philippines. More than half of Malaysians (56%) and 68% of Filipinos are very concerned or extremely concerned about their financial situation. The majority of Malaysians (67%) and Filipinos (71%) are very to extremely concerned about the strength of their local economy.

Consumers from the Philippines are the most confident about their housing market with (68%) saying that they feel moderately to extremely confident about their housing market.

A resilient market of cautious consumers

Whilst the SEA economy continues to be fairly resilient to inflation, among consumers concerns about the economy and their household finances continue to linger. Consumers are trying to stay in control of their finances and cut down on expenses. This translates into a cost-conscious mindset and is driving changes in consumer behaviour. Consumers are more price-sensitive, looking for value-for-money, low-cost alternatives without compromising on quality.

Cutting back: Shifts in shopping behaviour

When we asked SEA consumers about the methods they are currently using to cut down on expenses, on average 57% are currently purchasing cheaper groceries to cut down on expenses and expect to continue this over the next six months. Around two-thirds of consumers from Indonesia (66%), the Philippines (64%) and Malaysia (63%) are likely to be doing this, whereas Vietnamese consumers are less likely to be doing so (41%).

Just over one-third (36%) of SEA consumers are switching to home/white label brands to cut down on expenses and expect to continue to do this in the next six months. Consumers in Vietnam are less likely to be doing this (26%) compared to consumers in the other markets, particularly Singapore (45%) and the Philippines (44%).

Markets such as the Philippines, where household finances and the economy are a more common concern, are more likely to have switched and plan to continue buying cheaper groceries and home/white label brands. On the other side of the spectrum, countries with lower concern for their financial situation such as Vietnam are less likely to have switched to and plan to continue buying home/white label brands.

Lifestyle changes

Cost-of-living pressures are also having an impact on the lifestyle of SEA consumers, as just over two-thirds (68%) said that to cut down on expenses they are cooking more meals at home and expect to do so in the next six months. This is highest in the Philippines (79%) and Indonesia (77%). Almost half (49%) of SEA consumers is dining out less frequently to cut down on expenses and expect to continue this near term. Only consumers in Vietnam are less likely to agree to this (39%). Across SEA, almost half (48%) are also dining out at cheaper establishments and more than 2 in 5 are cutting back on food delivery and expect to continue in the next six months.

Consumers are cutting back on most categories over the next 6 months

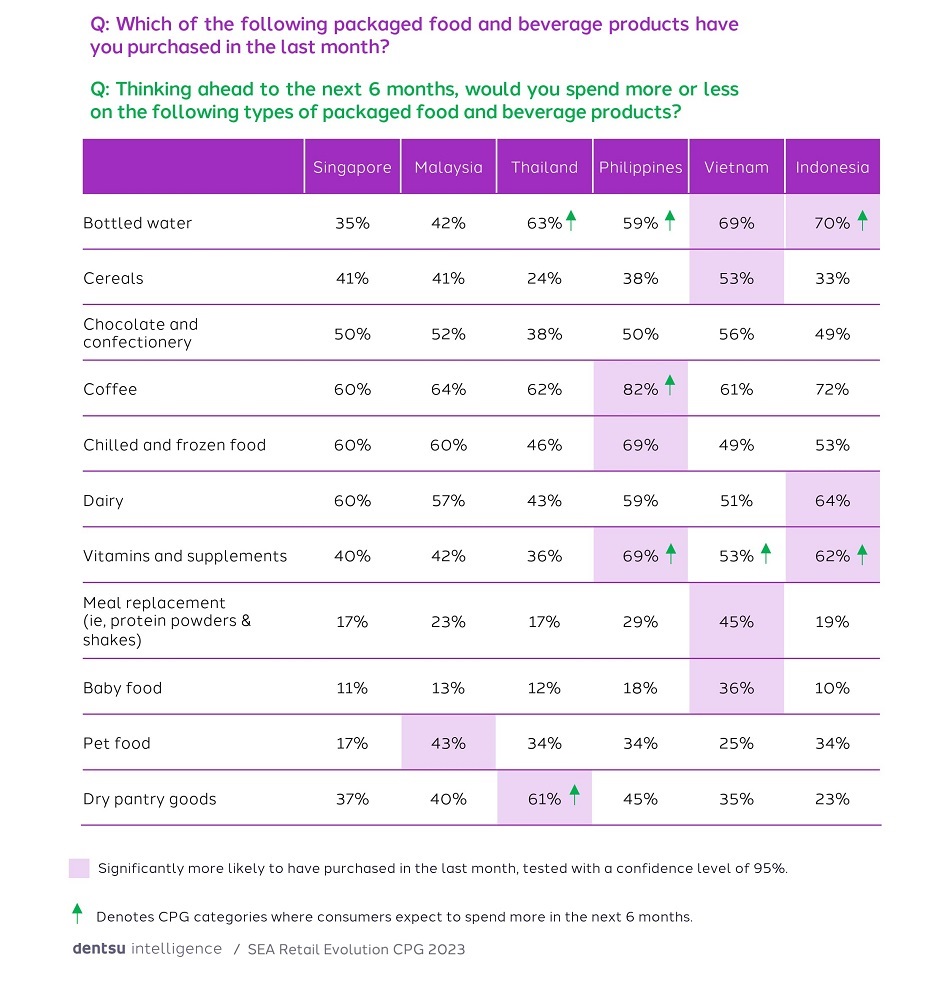

dentsu looked at what consumers are currently buying based on purchases reported over the last month and were able to identify items certain markets over-index on (shaded boxes in the table below), meaning that consumers in those markets were more likely to purchase those items than consumers in other markets. Additionally, the data also shows that consumers in SEA are planning on cutting back on all CPG categories in the next 6 months, except for the categories showing green arrows.

Consumers were asked: Q1: Which of the following packaged food and beverage products have you purchased in the last month? Q2: Thinking ahead to the next 6 months, would you spend more or less on the following types of packaged food and beverage products?

Share of budget and top drivers of purchase

On average SEA consumers allocate 27% of their income in an average month to groceries. Compared to the other markets, Indonesia spends the highest proportion of their income on groceries (43%). Consumers across SEA estimate that the allocation of groceries as a percentage of their income will slightly decrease over the next 6 months.

The top attributes that influence choice when making a purchase decision are quality and price. However, the importance of these attributes varies by country. Our survey shows that price is the top attribute to influence purchasing decisions in Singapore and Malaysia.

Quality is the highest attribute to influence purchasing decisions in Thailand, The Philippines, Vietnam and Indonesia. Price and quality are not the sole drivers of purchase for SEA consumers as convenience; value; ingredients/ materials; trust in the brand to do what is right; reputation of the company; transparency; values; supply chain; and ‘trendiness’, ‘coolness’ or ‘popularity’ of the brand or product also play a role.

Whilst the consumer outlook for the next 6 months is one of cautious, rational spending, consumer brands can remain competitive by proactively seeking to meet consumers’ preferences, such as by creating affordable sustainable products or introducing premium or unique products, such as hyper-local or artisanal ranges of their existing products.

To access the entire report, go to: https://www.dentsu.com/sg/en/reports/thought_leadership_retail_evolution_sea

References

1. Bain & Company 2023. Hoppe Florian, Baijal Aadarsh, Chang Willy, Chadna Sapna, and Wai Hoong Fock 2023. ‘e-Conomy SEA 2023.’ Available at https://www.bain.com/insights/e-conomy-sea-2023/#:~:text=SEA%20has%20weathered%20global%20macroeconomic,has%20come%20down%20to%203%25

2. BCG 2021. Meyer Michael, Tan Michael, Vohra Rohit, McAdoo Michael, and Min Lim Kar 2021. ‘How ASEAN can move up the manufacturing value chain.’ Available at https://www.bcg.com/publications/2021/asean-manufacturing

3. Statista. ‘Size of the middle-class population in Southeast Asia from 2000 to 2020, by selected country’. https://www.statista.com/statistics/1309353/sea-middle-class-population-size-by-country

4. McKinsey & Company 2021. Razdan Rohit, Yamakawa Naomi, Francois Matthieu, and Seong Jeongmin 2021. ‘The shifting consumer packaged goods market in a diversifying Asia.’ Available at https://www.mckinsey.com/featured-insights/future-of-asia/the-shifting-consumer-packaged-goods-market-in-a-diversifying-asia

6. OECD 2023. ‘Economic Outlook Southeast Asia China India’. Available at https://www.oecd.org/dev/asia-pacific/economic-outlook/Overview-Economic-Outlook-Southeast-Asia-China-India.pdf